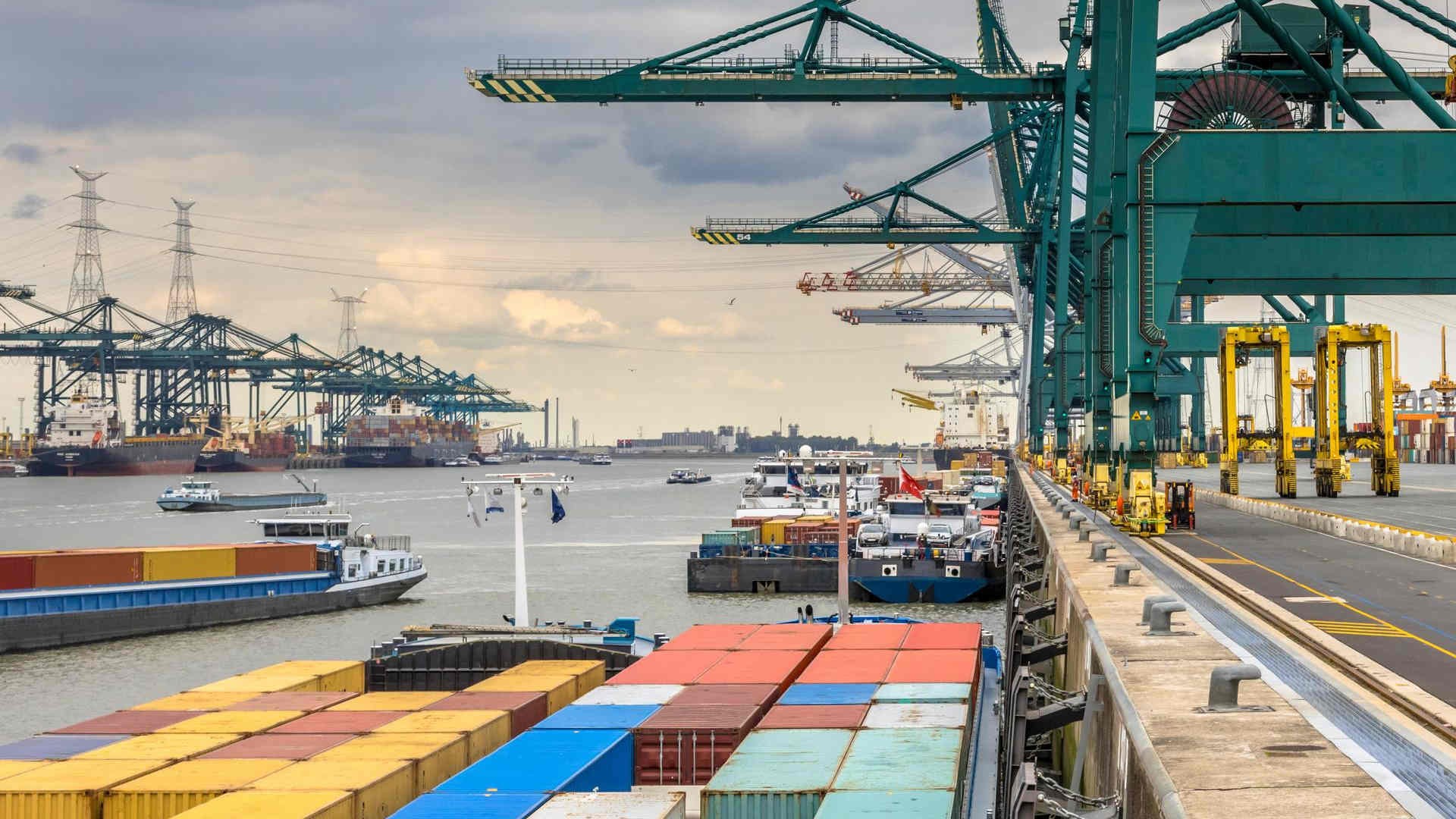

Large European port terminals remain affected by recurring constraints, including limited space, outdated planning, congested transport links, strikes, drought, and snowfall.

These issues contributed to extended waiting times for ships throughout the previous year, and market analysts expect such disruptions to persist into 2026.

They note that the causes vary frequently, ranging from labour actions to fluctuating river water levels, with both high and low levels inhibiting vessel movements at different times.

Infrastructure pressures continue to limit efficiency

Recent snowfall has produced new operational challenges in key hubs such as Rotterdam and Hamburg.

Maersk reported that delayed rail movements and slippery roads increased waiting times for both inbound and outbound cargo, adding to congestion at several terminals.

Efficiency is further constrained by the tight relationship between port operations and inland transport, with ports like Antwerp and Hamburg reliant on overland movements to destinations including Berlin and the Czech Republic.

Market analysts highlight that deteriorating infrastructure across parts of Europe, particularly worn motorways, ageing bridges, and decades of underinvestment in the rail system, continues to hinder port performance.

The situation is particularly restrictive on a continent where port activity is highly dependent on reliable hinterland connections.

Limited transparency and slow automation progress

A global ranking of container terminals was recently introduced by the Norwegian classification society DNV, assessing performance and the degree of automation.

Dr Shahrin Osman, business developer at the organisation, describes insufficient investment in Europe compared with Asia, where port authorities have committed significantly more capital to automation and advanced technology.

He attributes part of the shortfall to fragmented cooperation between port authorities, terminal operators, unions, and employer groups, which complicates and delays necessary development.

Osman comments that shipping companies continue to express frustration over the lack of transparency surrounding long-term European port expansion and upgrade plans. Without clear visibility of intended improvements to reduce waiting times and increase productivity, companies face difficulties in planning and fleet decisions.

“It’s hard to see the light at the end of the tunnel when you don’t know the plans for how port authorities intend to reduce waiting times and increase productivity at terminals,” he says.

In recent years, several major shipping companies have invested in European container terminals.

MSC has acquired a share in Hamburg’s largest container terminal, HHLA, while Hapag-Lloyd has expanded through investments in domestic ports and facilities in Le Havre, Genoa, and Salerno.

Similarly, Hamburg's terminal EUROGATE and CMA CGM's port arm CMA Terminals have entered a partnership, where the liner gets a 20% stake in the EUROGATE Container Terminal Hamburg. The two parties seek to support the terminal’s planned Western Extension.

Analysts believe that the limited available land in Europe means future investments will focus heavily on improving the efficiency of existing sites.

Rising labour costs and a worsening shortage of workers have made automation more urgent, with expectations of increased spending on AI systems, autonomous vehicles, and remote-controlled operations.

While unions have traditionally opposed automation, analysts observe that resistance has eased as labour shortages become more visible.

Red Sea reopening raises risks for European feeder operators

Feeder and short-sea carriers are expected to face renewed challenges following the reopening of the Red Sea, with congestion pressures likely to intensify.

Constantin Baack, chief executive of MPC Container Ships, states that the first impact will be broader congestion across networks, which will influence feeder services.

North Sea Container Line chief executive Bente Hetland notes that congestion will affect all companies operating in Europe, regardless of whether they use the Suez Canal, because European terminals have not received the investment needed to expand key locations or improve efficiency.

She explains that trade growth has outpaced the capacity of existing terminals, prompting her company to prepare multiple contingency plans. Smaller carriers without their own terminal infrastructure are expected to encounter greater difficulty securing port access as competition for limited slots increases.

“For small niche players that don’t have big volumes, it’s more difficult to get the priority in the ports,” Hetland says.

Baack observes that only a limited number of ships have begun transiting the Red Sea, and primarily those sailing under Danish or US flags for Maersk.

Hetland, however, expects that competitive pressures will lead more carriers to return gradually to the route, as companies may feel compelled to follow early movers to remain competitive.