As global commerce continues to evolve, the efficiency and capacity of US marine terminals are increasingly vital to supporting international trade and economic growth.

This report traces the development of American ports from their initial embrace of containerisation to the complex challenges and opportunities they face today, highlighting the influence of technology, labour practices, and operational strategies on their productivity and future prospects.

The development of US port containerised facilities

After the initiation of containerised ocean transportation in 1956 by Malcolm McLean and his company Sea-Land Service, ports in the US needed to develop facilities that could support this new mode of ocean transportation.

Containerised movement of ocean cargo is 25 to 30 times as productive as the pre-existing breakbulk system. In 1956, one labour gang of stevedores could process about 20 to 25 tons of cargo per hour. With containerisation operations, it became 500 to 800 tonnes per hour with one crane, a gang and associated equipment.

Today, basically all the US merchandise imports and exports move in containers and are processed through about 20 ports, which handled approximately 56 million containers in 2024.

Stevedore labour

Stevedore/port labour is an integral part of all facilities, not only because they are required for the facility to function, but also because they have a critical influence on the future of all port facilities in the US.

Almost all containers that move into or out of the US are handled by members of 2 unions: The ILA (International Longshoremen’s Association) covers the US East and Gulf coasts, and the ILWU (International Longshore and Warehouse Union) covers the West Coast.

To understand the attitude labour brings to the operation of US port facilities, it is helpful to understand what happened to stevedore labour when ocean transportation moved from breakbulk to containerised operations.

In the port of New York & New Jersey in 1955, the ILA had approximately 40,000 members in breakbulk operations. Today, while moving at least 3 times as much cargo, there are about 6,000 members. The workforce is 85% smaller but handles 3 times as much cargo. Containerisation devastated the stevedore union workforce in the US.

Given that both unions believe that technology and automation will eliminate jobs and their interest in protecting high salaries, both union contracts contain language that restricts or bans the use of automation technology. These restrictions on automation, while not a significant issue now, will eventually become especially important when US ports need to add capacity.

Current terminal operations

The US marine terminals have several characteristics that are different from those in the rest of the world.

US port operations are unique in how chassis are handled. The US is the only market in the world where carriers (and now intermodal equipment providers) supply chassis. In the rest of the world, the trucker supplies the chassis. The US is moving toward the trucker chassis model, but chassis still complicate the operation of US ports.

Most ports in the world operate on a 24/7 basis. US ports do not, in part, because of the high cost of labour. US port terminals generally operate 5 days per week, with occasional Saturday operations, for a total of 70 to 90 hours per week. 24/7 operations total 168 hours per week.

Many ports in the world operate automated facilities. The US does not have any except for several facilities scattered around the country.

At US ports, the heavy cargo direction is inbound (imports), meaning import cargo volumes are higher than export cargo volumes. The US is extreme in this regard and imports 4 times as many containers as it exports.

This complicates operations based on the need to store and process empty containers. Heavy import volumes make it difficult for these ports to be as productive as heavy outbound ports, like almost all the ports in Asia.

Another factor affecting a port’s overall operation and productivity is the number of facilities in the port. For example, the Port of New York & New Jersey has 6 facilities. Los Angeles has 8, and Long Beach has 7. Today, when a port is developed, it is with a single large facility.

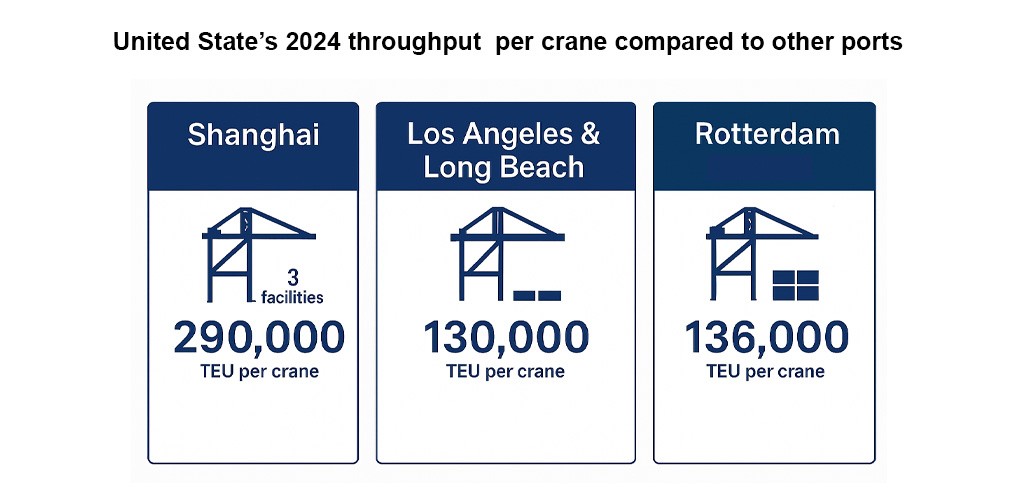

A good example of this is the Yangshan deep-water port in Shanghai. Yangshan (a single facility) has 103 (and rising) gantry cranes, while the port of Los Angeles & Long Beach has 15 facilities and 155 cranes. Single, more concentrated facilities can be more productive.

To give you an idea of what these various port factors and differences mean, the image below illustrates the overall productivity in a simple way: TEUs handled per crane.

Will there be sufficient terminal capacity in the future?

World and US trade will continue to grow in the future at about 2% to 4% per year. With this growth and given the political, labour and business environment in the US, it is uncertain how future marine terminal capacity needs will be met.

Marine facilities in the US are controlled by local or state authorities and not by a national agency. In most of the US, especially the West Coast and the Northeast, minimal terminal capacity has been added in recent years.

In fact, only one new facility has been added in the US since 2009. All other capacity additions have been via refurbishments, modernisations and some expansions of existing facilities. Impediments to the addition of terminal capacity include road traffic, noise, environmental impact, and alternative uses for the land (e.g. residential construction).

Other than along the southeast and Gulf coasts, pier 500 in Los Angeles and pier S in Long Beach, it is difficult to imagine a new facility being built or the footprint of an existing facility being expanded.

How can the US meet its future marine terminal capacity needs?

How can marine terminal capacity be added when new or expanded facilities are not an option? Fortunately, there are several ways to add capacity:

Modernisation: Updating cranes, other equipment, adding on-dock rail, business processes, and software.

Labour work rule changes: Changes to existing union labour work rules can facilitate more flexible and efficient operations, which will increase capacity. These can include the required number of workers for a task or worker classification requirements, shift timing changes, break timing and schedule changes are among the possibilities.

Hours of operation: The capacity of US facilities can be increased simply by increasing the hours of operation from the current 70 to 90 hours per week to some larger number up to 24x7.

Automation: Partial or complete automation of existing facilities can increase the capacity of existing US facilities. Automation can cover 3 parts of terminal operation:

- The move of a container to or from the vessel.

- The movement of containers into and out of the yard/stacks where containers are positioned as they await movement to the vessel or out of the facility.

- The gate where containers enter or exit the facility via truck.

The area of most significant potential is in the yard/stacks. The capacity of the yard/stacks can be increased by up to 50% by moving to an automated system.

One drawback of automation is that it is very expensive. The cost of operating an automated system can be made prohibitive based on manning and labour agreements, so reaching a satisfactory agreement with any union involved is critical.

In summary, the evolution of US marine terminals reflects a dynamic interplay between technological advancements, labour relations, and operational necessities.

As the industry continues to adapt to shifting trade patterns and modernisation challenges, the ability to balance efficiency, capacity, and collaboration among stakeholders will remain crucial for ensuring the continued vitality and competitiveness of American ports in the years ahead.