A recent study by maritime analysis firm Sea-Intelligence highlighted the evolving nature of the maritime industry.

The firm looked into the changes in market shares of the largest 10 container carriers over the past 15 years, during which significant transformations occurred.

From 2010 to 2015, the sector experienced a substantial increase in capacity due to the introduction of ultra-large container vessels and the formation of mega-alliances.

This period was then followed by one marked by numerous mergers and acquisitions, reshaping the competitive landscape of container carriers.

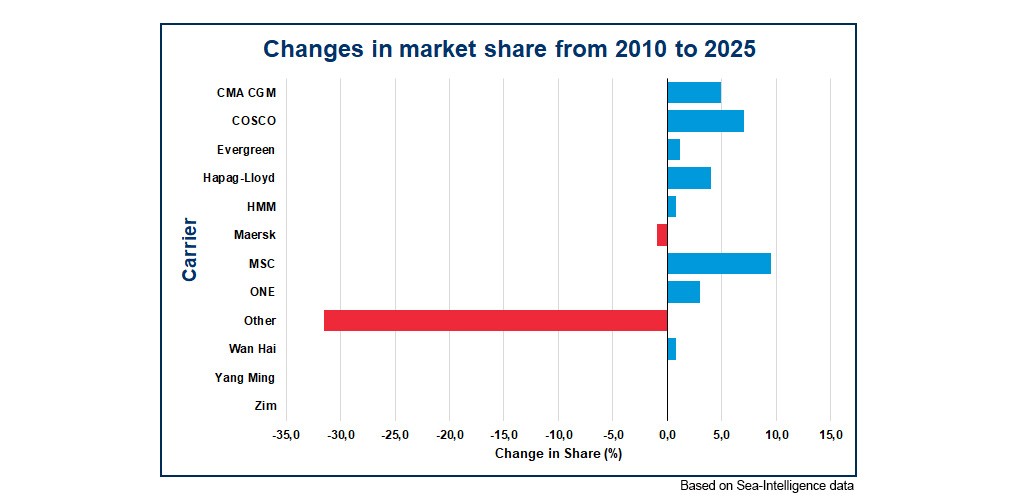

The study found that the top 10 carriers have seen considerable growth, primarily at the expense of other carriers.

"The consolidation in the container lines from 2010 to 2025 has seen the current top-10 carriers go from 55% to 86% market share," says Sea-Intelligence.

A significant observation is the decline in market share for Danish carrier Maersk, which has lost 0.9 percentage points over the past 15 years.

This decline occurred despite Maersk's acquisition of Hamburg Süd in 2017, which had a market share of 2.9% at the time.

Meanwhile, the study revealed that Swiss-Italian liner MSC emerged as the largest beneficiary throughout that period, with its gains nearly mirroring the losses experienced by Maersk and COSCO.

According to Sea-Intelligence's 2025 data, the approximate market shares for the top five carriers sit as follows:

- MSC at 21%,

- Maersk at 14%,

- CMA CGM at 12%,

- COSCO at 10%,

- and Hapag-Lloyd at 8%.

For the other carriers, HMM, ZIM, and Wan Hai have also shown notable market share gains, considering their relatively smaller sizes.