CONTAINER carriers have substantially ramped up capacity on intra-Asian trades over the past year, with Chinese lines among the most aggressive expanders, fuelled by manufacturers’ urgent push to establish overseas production bases amid escalating trade tensions.

The surge reflects both the region’s booming commerce and the strategic cargo diversions reshaping global supply chains, as companies scramble to navigate geopolitical headwinds.

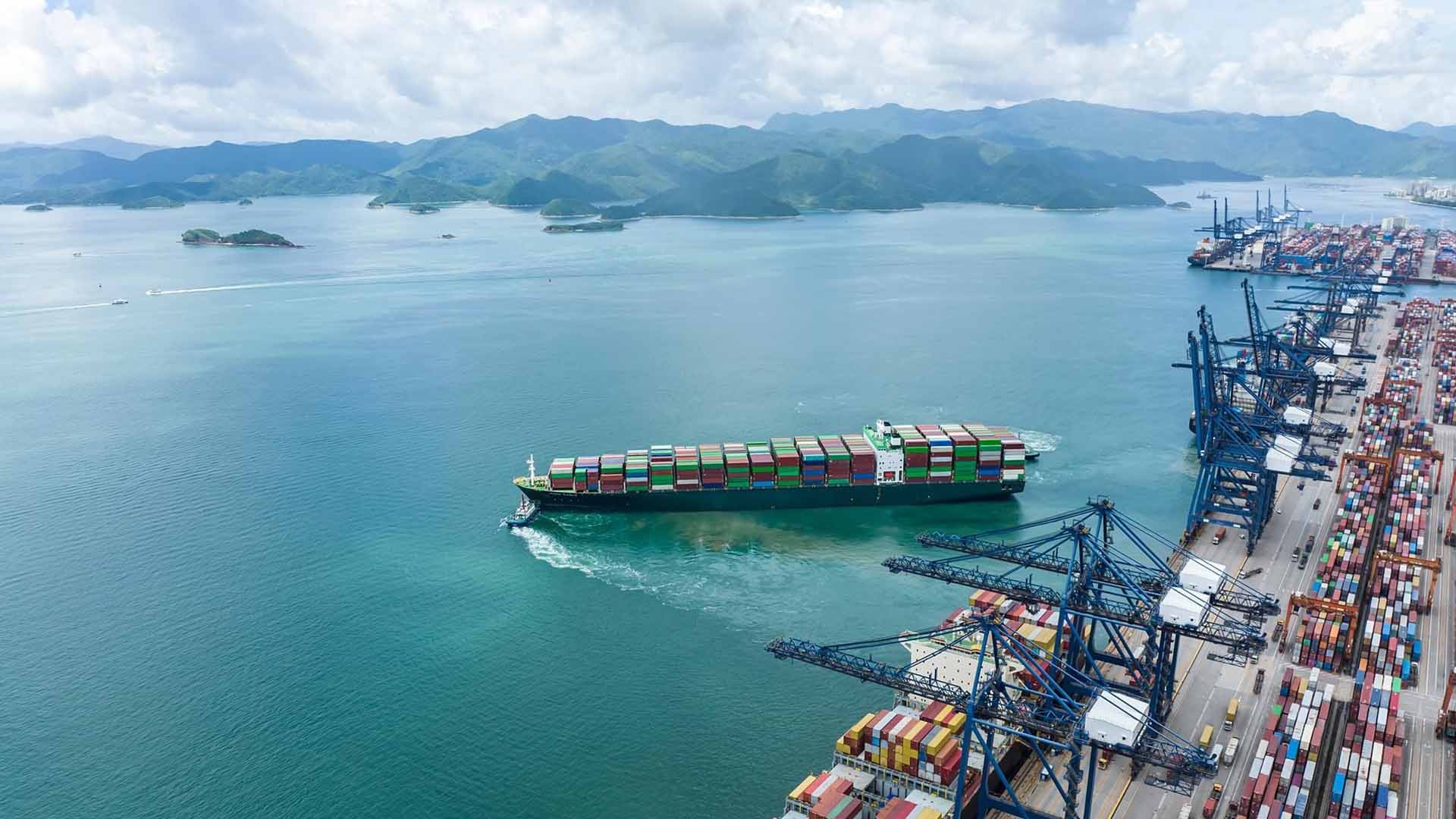

According to Alphaliner data, total intra-Asian capacity excluding domestic trades surged 12.8% year on year to nearly 2.4m teu, as of August 1.

Maersk led this expansion, adding over 100,000 teu in 12 months and narrowing its gap with market leader Cosco Shipping to under 2,500 teu. Its alliance partner Hapag-Lloyd achieved nearly 100% growth, albeit from a smaller base of approximately 16,000 teu.

“The main driver for the substantial growth of both carriers is the formation of the Gemini Cooperation, which saw the lines operate significantly more regional shuttles in Asia, to cater to its ‘hub and spoke’ concept,” Alphaliner said.

Maersk stated that this was both to complement the Gemini network and to “meet the evolving needs” of its customers for growth in the region.

Smaller Chinese carriers also posted impressive gains. China Merchants-owned Sinotrans Shipping expanded capacity by 35%, while Ningbo Ocean Shipping surged 51%.

Ningbo Ocean, part of state-owned Zhejiang Seaport Group, recently announced plans to establish two Singapore subsidiaries to invest in and operate four 2,700 teu and four 4,300 teu newbuildings, respectively.

Meanwhile, Singapore-based Pacific International Lines, which maintains close ties with China, achieved a remarkable 116% growth. This increase largely stemmed from deploying three 3,600-3,900 teu vessels on the North China-Indonesia ‘NCI’ service, launched in June with HMM and X-Press Feeders, according to Alphaliner.

The “China+1” strategy has gained momentum among manufacturers and brands since US president Donald Trump launched his trade war against “the world factory” nation during his first term.

Southeast Asian nations have become key alternatives for finished goods exports while relying on Chinese imports for raw materials and intermediate products.

Trump’s re-election and his broader tariff measures against trading partners have accelerated this trend, and is creating increasingly complex global supply chain reconfiguration.

“Trade growth between China and Southeast Asian emerging economies is the primary driver behind intra-Asian capacity expansion,” said an executive from SITC, the Shanghai-based carrier ranking sixth in the intra-Asian market.

Its capacity grew 8% over the past year, though it ranks among the top three by vessel count alongside Maersk and Cosco.

Currently, US tariffs on China remain substantially higher at 54% compared to major Southeast Asian economies, with limited prospects for significant reduction despite ongoing negotiations.

However, uncertainty persists. One case in point is the Trump administration’s threat to impose extra ‘transhipment’ duties, targeting goods made in China — or largely manufactured there — that are re-exported to the US through third countries. The detailed rules have yet to be released.

Some industry experts believe this will increase factory relocation uncertainty and potentially dampen US demand, subsequently affecting Sino-Asian trade growth. Others disagree.

Yan Hai, transport analyst at Shanghai-based SWS Research, argued that the exorbitant transhipment tariffs are forcing Chinese companies to accelerate overseas production transfers, increasing local value-added content to reduce tariff exposure.

For shipping, this means sustained demand for raw materials, intermediate goods and equipment beyond finished product shipments.

“Previously, Chinese companies went overseas for better opportunities; now it’s for survival,” Yan noted.

Midea, one of China’s largest home appliance makers, said in its first-half 2025 earnings report that it now operates 22 R&D centres and 41 major manufacturing bases across more than a dozen countries. In the second half, the company plans to launch construction of a new plant in Thailand, continue investing in its Indian facility and bring its Brazil plant into operation.

While underscoring the company’s extensive overseas presence, these moves also highlight the risks of its chosen investment destinations, given the US tariffs of up to 50% on India and Brazil.

“But they must make choices, diversifying manufacturing locations to spread tariff risks — overall, this is a sensible approach,” said Jayendu Krishna, head of Drewry Maritime Advisors.

Recent Chinese customs data clearly demonstrates this diversification has continued.

The country’s exports to the US in dollar terms fell 15.5% in the first eight months, with August alone declining 33%.

Conversely, exports to Asean nations rose 14.6% over the eight months, led by Thailand’s 22.9% and Vietnam’s 22.1% growth. African exports also soared nearly 25%.

Linerlytica data shows vessel capacity deployed on Far East-Africa trades increased over 50% year on year as of September 8, the highest among all routes.

Linerlytica also provides more detailed fleet deployment analysis by breaking down Asian trades into intra-Northeast Asia, intra-Southeast Asia and NSA-SEA segments.

Focusing on the largest NSA-SEA trade, many carriers show more pronounced capacity expansion.

Cosco Shipping grew nearly 10% compared to 3% under Alphaliner’s methodology. STIC expanded 16%, Sinotrans 66%, while Ningbo Ocean’s fleet of 13,599 teu in this niche started from zero deployment in September last year.

In addition, Hapag-Lloyd and PIL almost quadrupled their capacity, while HMM also recorded an impressive 135% increase.