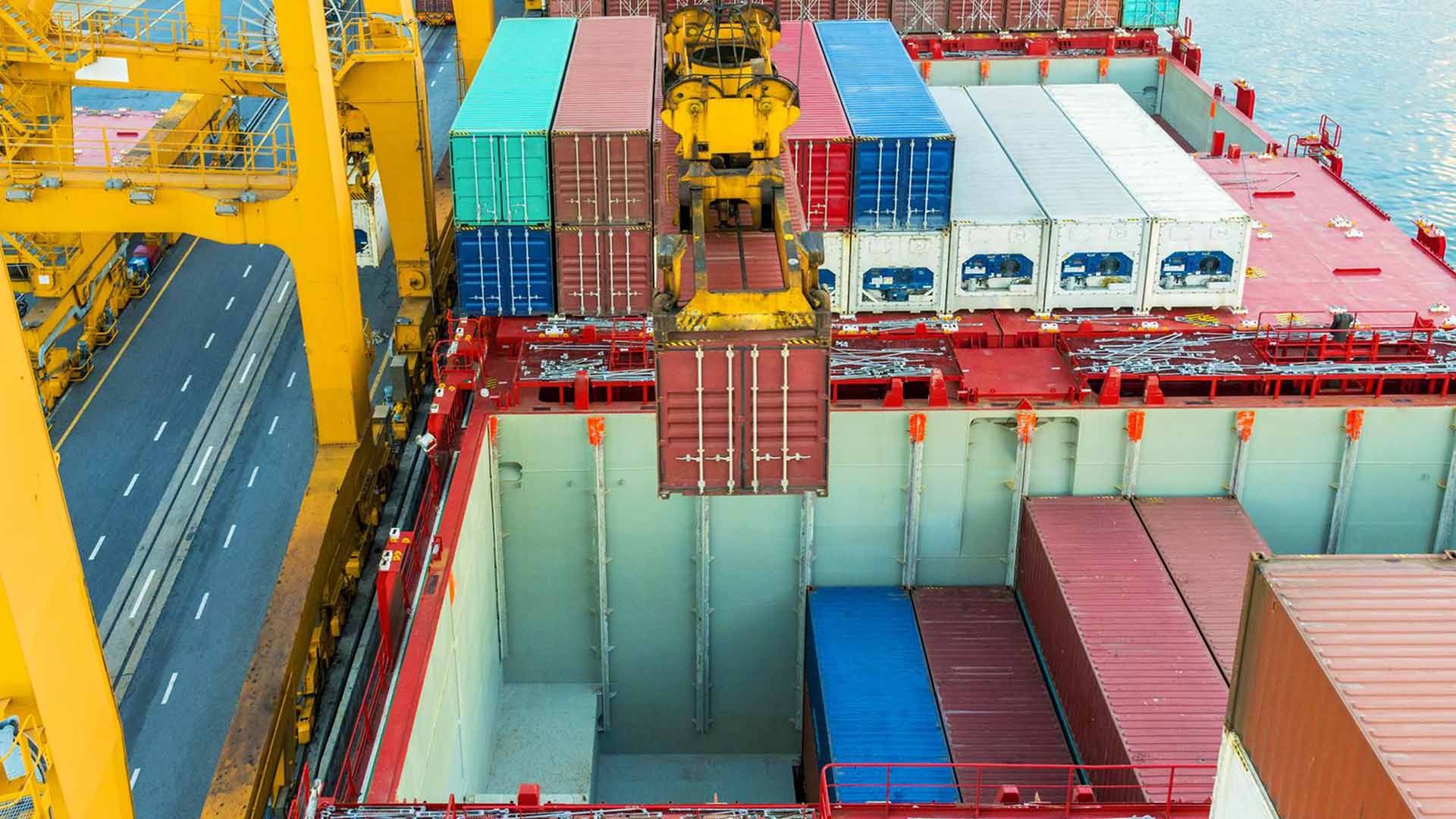

WEST Africa is fast emerging as an unlikely yet increasingly credible destination for liner shipping’s ultra-large containerships.

Long viewed as a secondary market, the region’s recent infrastructure upgrades and strategic positioning have turned it into a viable ULC deployment zone, while the rerouting of Asia–Europe traffic around the Cape of Good Hope has granted the industry a timely testing ground.

As carriers seized the opportunity to trial their biggest vessels in West African waters, the results have been nothing short of transformative.

With terminals now routinely handling ships above 20,000 teu, the region has demonstrated its readiness to support the industry’s biggest assets, while rising demand for containerised trade make it a natural candidate for long-term ULC deployment.

So how did we get here?

The answer begins with demand. Figures from Container Trades Statistics show that West Africa’s box trade has grown by nearly 50% in less than a decade — a growth trajectory that has outpaced global averages. This surge in volumes laid the commercial foundation for carriers to consider deploying ULCs, but it was infrastructure — not just market appetite — that has made it possible.

The turning point came in 2014, when Mediterranean Shipping Co, through its terminal arm Terminal Investment Limited, partnered with China Merchant Holdings to open Lome Container Terminal in Togo.

LCT, one of the few natural deepwater ports in West and Central Africa, was designed and built for the sole purpose of handling ultra-large tonnage. The facility was the cornerstone to MSC’s grand plan to rip up the rule book of how container trade operated in the region.

Speaking to Lloyd’s List, Dynamar shipping analyst Darron Wadey said that for West Africa the inauguration of LCT was similar to how the Daily Maersk product back in 2011 transformed the dynamics of liner alliances.

He explained how just before LCT opened, MSC launched its Asia–West Africa service with multiple regional port calls. But once Lomé became operational, MSC shifted all calls there, marking a significant shift. Previously, West Africa relied on direct or relay services — predominately from transhipment hubs in the West Mediterranean, such as Algeciras, Valencia and Tanger Med, and to a smaller extent South Africa.

“The moment that MSC put all their ships into Lomé, and Lomé only, they had to have a corresponding feeder network. So for the first time, this meant an organised hub-and-spoke system in West Africa,” said Wadey.

LCT had laid the benchmark for other carriers to explore the possibility of sending big ships to the region, and follow they did.

The success of MSC’s West African transhipment model paved the way for both Maersk and CMA CGM to upgrade their affiliated terminal networks in a similar vein.

Fast forward over a decade, five further facilities have since been set up in West Africa, in addition to LCT, to facilitate the handling of ultra-large tonnage, in which either line has a vested interest.

Maersk, through terminal arm APM Terminals, has three such terminals capable of handling ships of more than 14,000 teu, namely in Tema, Ghana, the Ivorian port of Abidjan and the Republic of Congo’s Pointe Noire. While in the case of CMA CGM, it has an invested interest at facilities in Kribi, Cameroon, and at Lekki in Nigeria.

In the year’s proceeding, LCT’s opening, 10,000 teu-14,000 teu ships became an increasingly common feature on carrier strings into West Africa as this procession of ULC-ready terminals came online, which saw Maersk and CMA CGM follow MSC’s lead with direct regional calls.

Like MSC, its European compatriots have adopted a regional hub-and-spoke model out of these hubs to serve the region directly rather than the conventional relay approach.

This rapid increase in tonnage deployment is impressive on its own, but the onset of Red Sea rerouting gave carriers a unique opportunity to trial their largest ships in West African waters.

As Asia-Europe trade shifted around the Cape of Good Hope, shipping lines seized the moment to conduct ad-hoc wayport calls for regional transhipment. These impromptu operations have offered a real-world stress test of West Africa’s ULC port infrastructure’s capabilities.

Maersk, for one, has looked to put its trio of terminals to the test, most notably in Abidjan and Tema, which offer the least deviation from the revised Asia-Europe route.

“What we’ve discovered is that you can also do transhipment on the west coast of Africa, rather than go to the Suez [Canal] and do it in the West Mediterranean, particularly in our facility in Ghana and the Ivory Coast,” Igor van den Essen, Maersk chief executive for Africa and Europe, told Lloyd’s List.

“It’s actually the very reason we built them… with a deeper draft that could receive large vessels and therefore is suitable for transhipment.”

For MSC this examination of its ULC fleet led to another big step change, whereby once again the Geneva-based line has looked to trailblaze its operations in the region.

In April this year, MSC revamped its Africa Express Service — the carrier’s principal Asia-West Africa offering — by deploying 24,000 teu ships on the loop, which calls not just Lomé, but also Tema, Abidjan and Kribi. MSC said at the time, the bold move was in response to surging Asia-West Africa trade and increasing customer demand for container services.

The Liberian-flagged MSC Diletta’s arrival in Lomé on April 23, 2025, marked the first call of a 24,000 teu ship in West Africa on the service. According to MSC, this milestone was a “turning point, ushering in an era of unprecedented shipping capacity for the region.” MSC Diletta (IMO: 9897004) and its sister 24,000 teu vessels have since become a permanent fixture on MSC’s Africa Express Service.

The indications too are that these ships are sailing into West Africa close to their maximum deadweight capacity. Although it cannot be determined whether vessels are arriving fully laden, this does at the very least prove the region can accommodate these ocean giants at their operational limits. Data from Lloyd’s List Intelligence shows recent callings of three MSC ships — MSC Michel Cappellini (IMO: 9929431), MSC Apolline (IMO: 9896983) and MSC China (IMO: 9936642) — all with a capacity close to 24,000 teu, into Tema with a draft of 16 metres and above, or close to their maximum of 16 m-16.5 m.

“They’re not going to put those ships on that service, if the service and facilities didn’t justify it,” said Wadey, noting how these boxship behemoths are now the predominant vessels plying the MSC loop.

Indeed, the average size ship currently operating this West African service is now up and above 21,000 teu. To put this into context, the largest ships operating the transpacific trade remain at 18,000 teu, but even these are few and far between and nowhere near dominating the fleet composition of any one service.

Maersk’s van den Essen said that what West African carriers are discovering is that this trade pattern “works”. However, what is more significant is what will happen when the Suez route is eventually deemed safe to pass.

“My expectation is that change in trade pattern will stick after the Suez Canal reopens… and that’s good news for West Africa,” he said, adding, that in the case of Maersk, it is actively looking at further facility upgrades and investment in the region.

If the trend does indeed “stick” then the positive impact on West Africa could also have the opposite effect on hubs that have traditionally relayed cargoes to the region, most notably in the West Mediterranean.

Wadey explained that the geographical cutoff point for route efficiency for Asian cargoes to West Africa via the Western Mediterranean lies around Conakry, Guinea. Ports north of here could effectively still benefit from being served by transhipment hubs in the Mediterranean if carriers choose to continue with direct Asian services.

However, if going direct to West Africa via the Indian Ocean and around the Cape of Good Hope, this would remove the need for transhipment further north. While it would still make sense to ferry transatlantic and North European cargoes south along the coastline to West Africa from the Gibraltar Strait, there is every chance these West Mediterranean transhipment hubs could lose a significant portion of Asia–Africa business, said Wadey.

While the full impact of these shifting trade dynamics remains difficult to quantify, there are signs that major West Mediterranean hubs like Tanger Med and Barcelona may already be losing West African trade. According to Wadey, these ports are currently absorbing additional transhipment volumes that would typically be handled by hub and spoke specialists in the East Mediterranean such as Gioia Tauro, Piraeus and Port Said. This temporary influx — driven by the closure of the Suez Canal — could be concealing a broader loss of Asia-Africa relay traffic.

Since carriers started sailing around the Cape, Lloyd’s List Intelligence data shows a notable drop off in service calls from West Mediterranean hubs into West Africa. In the third quarter of 2023, calls originating from the region totalled 69, whereas in the same three months of 2025 this fell to 41, a fall of more than 40%, according to Lloyd’s List Intelligence. In terms of capacity this represented a drop off of more than a third, or 34.6%.

Wadey observed that although this southbound traffic has declined, MSC’s decision to deploy its 24,000 teu vessels on the Asia-West Africa trade lane signals sustained demand.

“They’re not creating cargoes — transport doesn’t do that. Transportation capacity is a reaction to demand,” he explained.

This assessment is backed by the latest data from CTS. This shows volumes on the route surged by approximately 30% in the first half of 2025 compared to the same period last year, extending the robust growth trend for the trade of recent years.

The question now is whether history will repeat itself once more, with MSC’s rivals following its lead by deploying even bigger ships of their own, while committing to permanent direct calls into West Africa.

The infrastructure is in place, and, as van den Essen explained, now has a proven track record. Of note, West Africa is also one of the few regions where congestion has improved since the pandemic, a factor Drewry senior analyst Eleanor Hadland told Lloyd’s List is inherently linked to the region’s adherence to ULC design principals.

Demand too is lending its hand. While Asian imports have surged, all container traffic to West Africa has continued to grow above the market average in recent years, a feat Drewry expects to be repeated in 2025 with volumes climbing more than 9%.

Van den Essen is also encouraged by a renewed focus by governments in West Africa to unlock trade corridors to its vast hinterland and untapped landlocked markets, plus an emphasis on localised manufacturing to drive exports in a region heavily weighted by imports.

He is “optimistic” that containerised trade will continue to flourish in the coming years. Maersk has hedged its bets on the region’s fortunes to the tune of several hundred million dollars.

However, Maersk is not alone in seeing West Africa’s potential.

In addition to the five readymade box facilities designed specifically with ULCs in mind, is another two such projects looking to capitalise on this new trade dynamic.

Earlier this year DP World broke ground on a $1.2bn project to construct a new 1.2m teu container terminal in the Senegalese port of Ndayane, boasting an 840 m quay and 16 m berth depth to accommodate “the world’s largest containerships”.

Further down the line is the AD Ports-backed Noatum Ports Luanda Terminal, which will see Angola join the big ship club when it opens to commercial shipping in the second half of 2026.

For Van den Essen this growing competition in West Africa is a positive development, as it is proof of both the rising demand for container services and the need for continued investment. “Let me put it this way — we can’t do it all ourselves,” he said.

West Africa’s emergence as a key player in the ULC era marks a shift that not so long ago would be almost inconceivable. The region now offers a viable haven for the industry’s newbuild backlog, which is heavily skewed by a pipeline of ultra-large tonnage.

While it won’t singlehandedly solve the challenge of where all of these ships will be deployed, West Africa has firmly established itself as a credible and strategic option for carriers.