The reefer market faced several challenges during the pandemic years, but it proved to be resilient.

The year 2022 came with a new set of challenges after the start of the Russia-Ukraine conflict. However, the demand for perishable goods remained relatively robust.

The Reefer Shipping Annual Review & Forecast report published by Drewry in August of this year revealed that perishable cargoes moved by sea witnessed a slight fall in 2022, dropping from 138.7 million tonnes in 2021 to 138 million tonnes in 2022.

Of the seaborne reefer cargoes, fresh vegetables had the most impressive performance in terms of year-on-year growth. Their volumes exceeded 17 million tonnes in 2022.

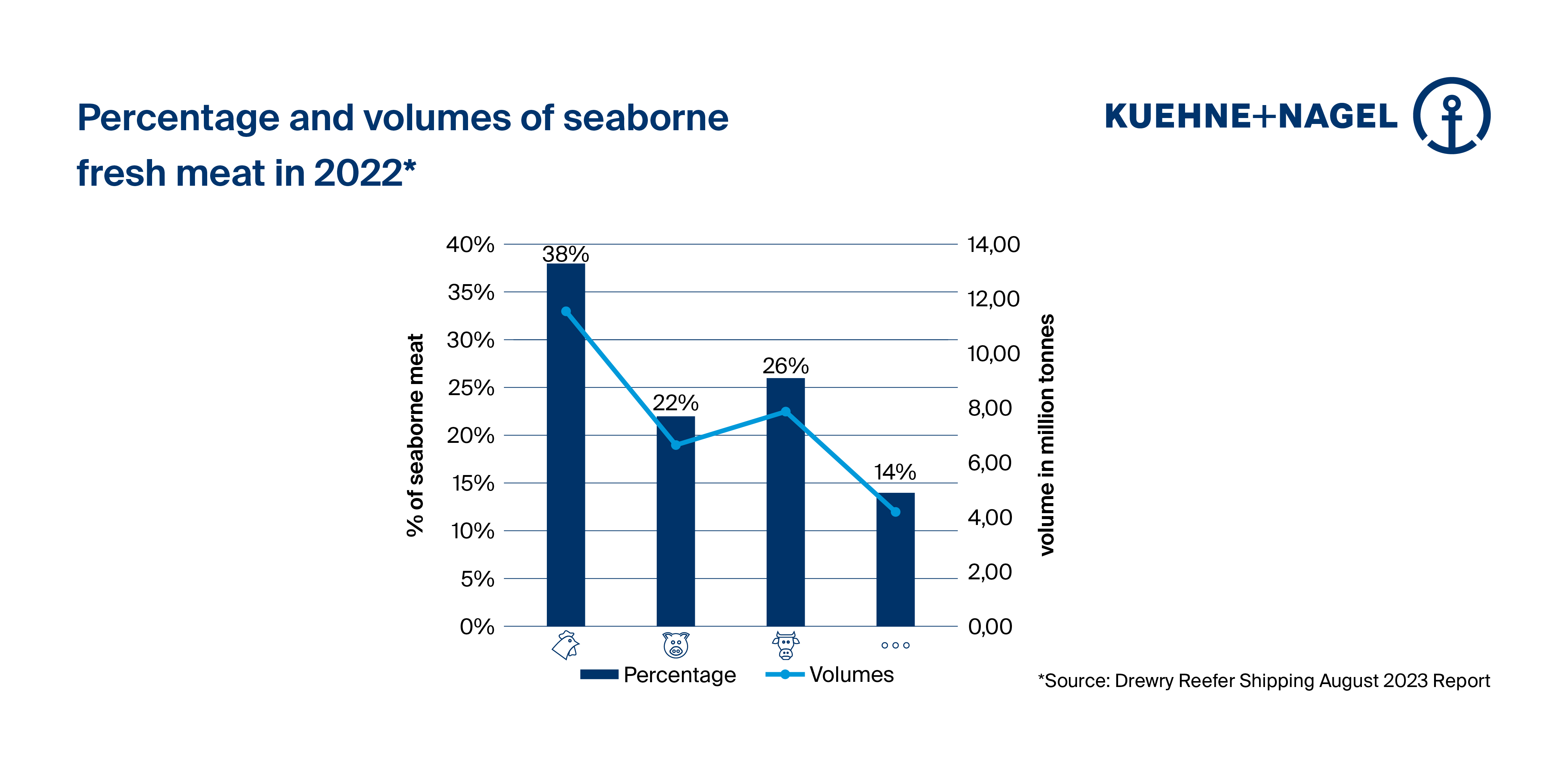

However, fresh meat and meat products remained the largest. This sector's overall volumes reached nearly 47 million tonnes last year.

Poultry was the most popular meat last year, constituting 38% of the volume.

Seaborne meat in numbers

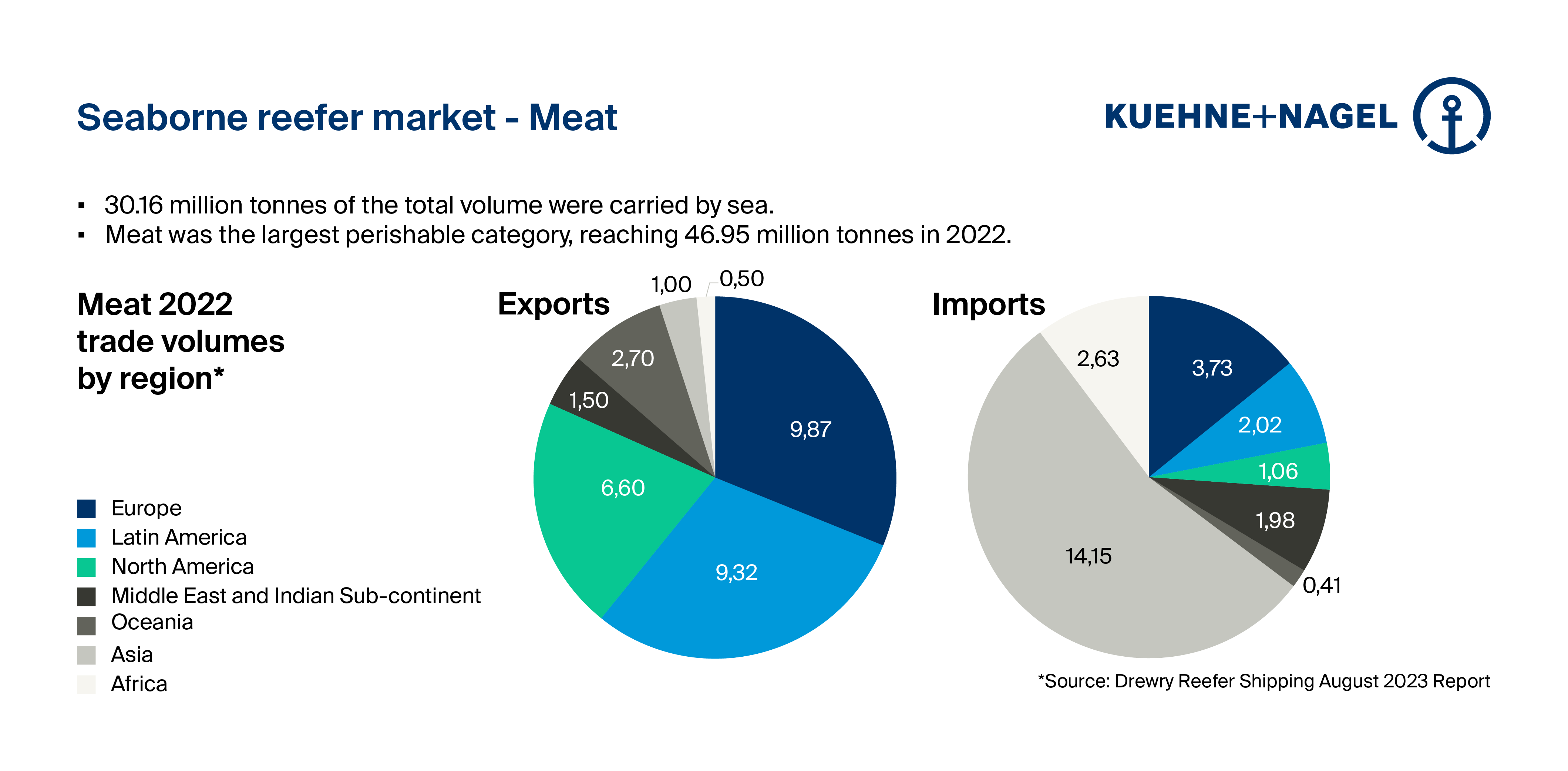

Despite slightly declining compared to 2021, seaborne fresh meat volumes reached about 30 million tonnes in 2022.

Asia was the largest importer of this commodity by sea (14.1 m tonnes), followed by Europe (3.7 m tonnes), according to the Drewry report.

Looking at the world’s regions, Europe was the largest ocean freight exporter of this commodity in 2022, as it exported nearly 10 million tonnes (nearly 31% of global seaborne volumes). This was followed by Latin America, which exported approximately 9 million tonnes.

However, on a country level, Brazil took the lead in 2022 as it had the highest volumes transported by sea (nearly 7.5 million tonnes). The United States was the second largest exporter last year, shipping about 5.5 million tonnes.

Trade lanes with the largest volumes

The trade lane that carried the largest volumes of this commodity in 2022 was the ECSA – Europe route. Volumes shipped between those two regions in 2022 reached 4.9 million tonnes.

Meat constituted 27% of the total commodities transported on this route. It is, however, not the main commodity that flows between the two regions, as it comes second to frozen fruit/juice (38%).

Kuehne+Nagel expert view

This market segment is witnessing several changes at the moment. Asian countries, and especially China, have been improving their domestic production of meat.

In the meantime, Europe's production decreased. The main reasons behind this include increased production in China and African swine fever in main producing countries, which is leading to a lower demand overseas and reduced European pork production.

Costs like energy and fuel also play an important role in influencing international competitiveness.

With some Asian countries opening again for European pork products, exports might increase slightly again, but not to the levels we had been seeing in the past.